Langley Township Debt: How It Grew, What It Funds, And What It Means For You

There has been a lot of talk about the Township's quickly growing debt. I hope this clears up a few points on this important discussion.

Township debt was a leading issue in the recent by-election. In this blog post, I look at official records to clarify what changed, what the debt pays for, and what it means for residents.

Did Township debt become one of the highest among B.C. mid-sized municipalities during this term?

Fact Check: True, relative to recent growth

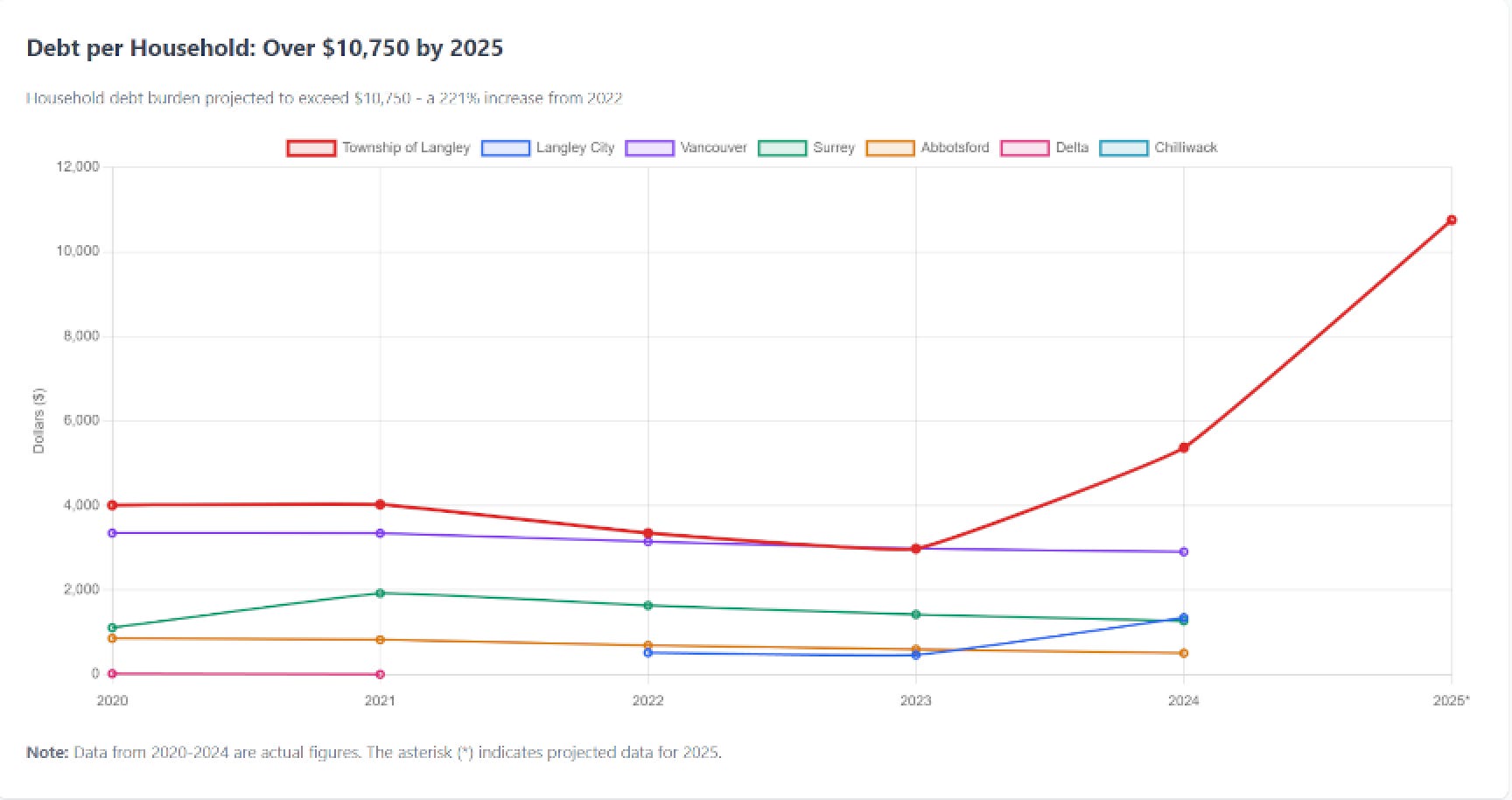

Langley’s 2024 Annual Report shows long-term debt and agreements payable of about $317 million as of December 31, 2024, up from $167 million the year before. The borrowing authorizations approved since 2023 total around $500 million in approved projects, though not all have been borrowed yet. On a per-person basis, Langley’s debt appears higher than that reported by municipalities such as Abbotsford and Coquitlam. Debt payments are currently expected to total about $23 to $27 million per year over 2025 to 2029. This appears to be about eight percent of the Township’s annual revenue base.

Is the rapid debt growth justified by population and infrastructure needs?

Fact Check: Maybe

Langley’s population is climbing quickly, with thousands of new housing units planned in Willoughby, Brookswood, and Willowbrook. The Township’s capital plans show that many borrowings are tied to water, storm, and transportation projects necessary to service this growth. For example, the Jericho Water Booster Station and Smith Stormwater Network are both funded through development cost charges. In that sense, borrowing allows construction ahead of fee collection. However, it appears that some loans, including the arena expansion and strategic land purchase program, are only partly covered by growth-related revenues and are currently projected to rely on general taxation.

Is the debt being used mainly for essential services?

Fact Check: Sort of

A significant portion of recent borrowing supports core infrastructure such as water supply, drainage, and major roads. These are traditional, defensible uses of debt. The remainder funds community amenities and policy-driven acquisitions, such as a multi-sheet arena expansion at the Langley Events Centre, Yorkson Park upgrades, and a $75 million land-bank for future civic use. These projects may enhance livability but do not produce operating revenue. Their debt servicing will draw on taxes unless offset by community amenity contributions. The analysis suggests that the mix of essentials and amenities makes the overall borrowing program broader than is typical for a single council term.

What this means for us

Debt service is now a fixed cost in the Township’s annual budget. As of 2024, the combined principal and interest payments are about $26 to $27 million per year. Property taxes and utility rates already incorporate these costs, and future increases may be needed if growth revenues lag. Each one percent increase in Langley’s general tax rate raises roughly $1.5 to $1.8 million in revenue, depending on the year. The Township remains well below the provincial borrowing cap set at 25 percent of eligible revenues. For 2024, the certified limit was about $77.7 million, and with existing and spring 2025 borrowings, annual servicing would total around $40 million—roughly half of that capacity. In my view, the Township’s financial flexibility appears to be much tighter than in past years.

Debt is a standard municipal tool, and using it for growth-related infrastructure makes sense. The key takeaway is that the pace and scope are notable. It appears the Township has roughly doubled its debt load in a single year. Our ability to manage this debt depends heavily on continued development and stable interest rates. If growth and developer contributions arrive as planned, the burden will remain manageable. If they do not, we may see higher taxes or slower new investment as the Township services the obligations already on the books.